In this month's Note Factory News, we would like to share a "sneak peak" from our new book on seller financing. This book is filled with valuable information for both the passive "hands off" investor and the "do it yourself" investor interested in creating his/her own notes. For the "hands off" passive investor, it will provide you with a "nuts and bolts" view of how your investment is working and give you a better understanding of exactly how your returns are being generated. For the "do it yourself investor" it will provide you with the framework you need to begin creating your own notes.

The following excerpt focuses on the reasons why one should consider to begin creating and/or investing in real estate notes. If you would like to pre-order a copy of the book, please email Mitchell@thenotefactory.com. Subject line "Book Pre-Order." We hope you enjoy.

Why Seller Financing?

1. Owners VS. Renters: We met a wealthy man recently who asked what we did for a living. We explained that we are in the business of creating and selling real estate notes for ourselves and private investors. During the conversation he told us about a friend that had accumulated over 150 rental homes during a 10 year period and ended up having to file bankruptcy! What started out to be a plan to build wealth turned into a financial nightmare!

We can’t tell you how many people that we have come across in the past 10 years that wanted to invest in real estate and chose the rental home route. Almost all of the people we have talked to say something like this “I used to have rental properties but I never really made any money and just could not stand the headaches of tenants any longer, so I sold my homes”. Even people that had property management companies often say the same thing. Just because there is a property manager, does not mean you don’t have to write checks for air conditioners, new roofs and new stoves because the last one got stolen by the previous tenant. We managed our own portfolio of rentals for several years and it went about as perfect as we could have hoped for. When it was all said and done, we did get some appreciation on our properties and the tenants did help us pay our mortgages BUT…. the routine maintenance and the vacancies between tenants ate up most of the profit. Rarely do we meet anyone who talks about how much money they are making on their rental properties, especially when they have a mortgage on the home.

When you owner finance a property, the home owner fixes their own toilet, air conditioner etc. Also, assuming the home owner keeps paying, the vacancy issue goes away. On a typical rental property, most people collect a deposit in the amount of ONE additional monthly payment. BIG DEAL! Most “deposits” are not enough for the tenant to care about when financial trouble comes their way. Let’s say we have a house that would rent for $1000 per month. On a typical rental, most people would collect a $1000 or even a $2000 deposit. On the same property, if you were to owner finance it you would collect about $10,000 from the buyer in the form of a down payment. A buyer that has “skin in the game”, is much less likely to flake out when things get a little tough. Most people will beg, borrow or steal the money to keep a roof over their head if they have $10,000 in the game. $10,000 has seemed to be the magic number to avoid most payment problems on homes valued under $100,000. If you can’t get a solid $10,000 down payment, we would not recommend offering owner financing terms to a buyer.

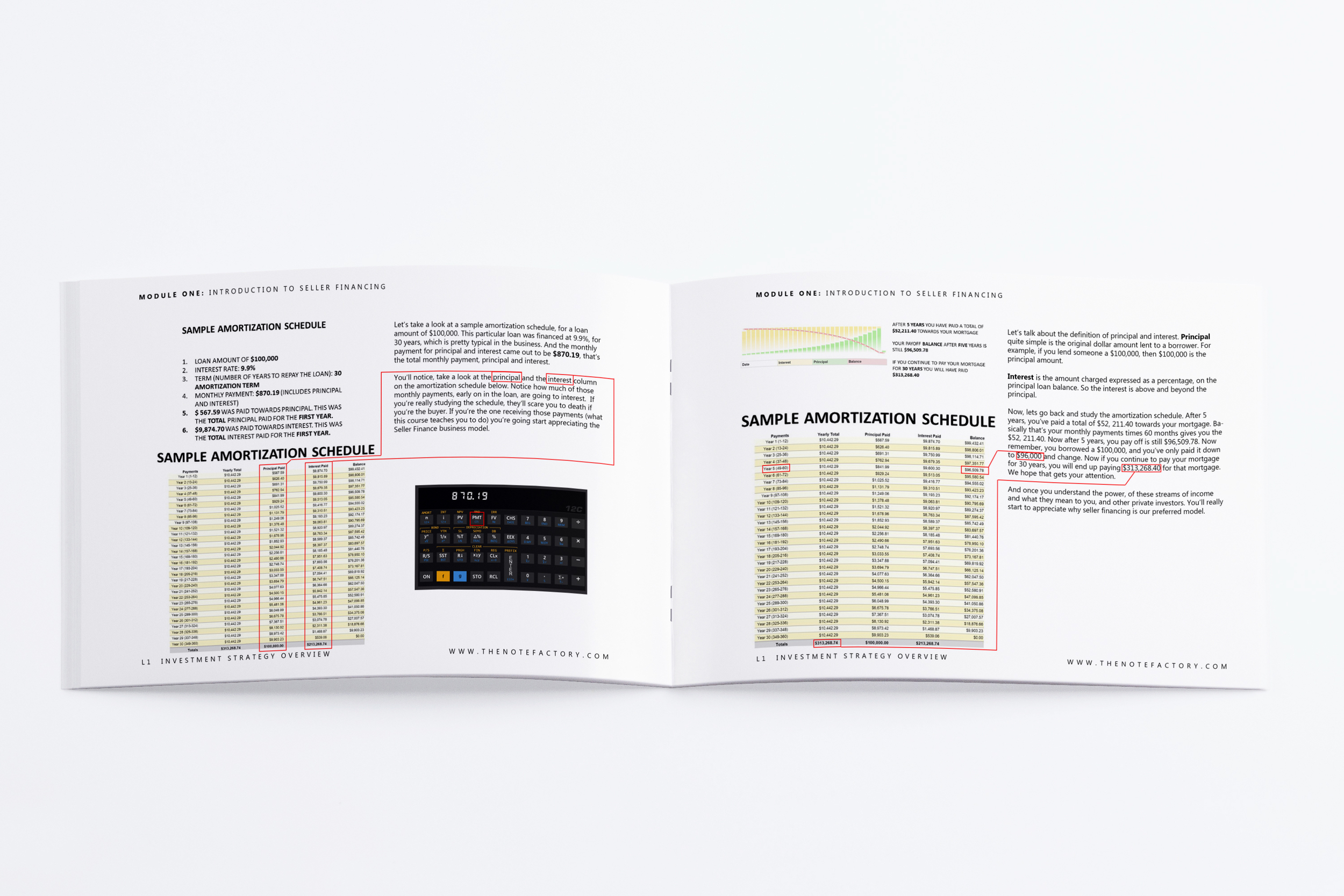

1. Amortization schedule: Our friend Joe stopped by our office one day and asked if we would review his paperwork from a house he had financed about 10 years ago. We looked over the file and saw that he paid $65,000 for the house and paid $5,000 down. Joe financed $60,000 over 30 years and the interest rate was 10.9%. Joe wanted to know how much he still owed. He had guessed about $35,000 to $40,000 because he had been paying on the house for about 10 years. When we worked up an amortization schedule for him, we said “Joe, you still owe a little over $55,000”. Joe said “that can’t be right! I have been paying on this house for 10 years”! We double checked the numbers and verified that they were correct. Joe paid 10 years of payments at $566.86 per month for a total of $68,023.20. He only paid $4,717.22 in principle in 10 years and he still owed $55,282.78. Read this paragraph again and again. He made payments for 10 years and on average paid less than $500.00 PER YEAR towards principle. That is the beauty of the amortization schedule. When you offer owner financing, YOU get to collect all of that interest. In the above scenario, you would have collected $63,305.98 in interest during the first ten years of the loan and still be owed $55,282.78 on an original loan of $60,000. Are you starting to see the unlimited potential of the owner financing business model?

2. Appreciation and Principal pay down: Like a fine wine, as time goes by, a steady paying note gets better with age. Notes that have been performing for a period of time are called “seasoned” notes. In a “normal” real estate market, if there is such a thing, homes generally appreciate or increase in value over time. As a note is seasoned, the underlying collateral usually increases in value each year. At the same time, the amount owed on the home gets reduced each year as the homeowner continues to pay their monthly payments. The moral of the story is that as the note holder, your risk is reduced each year. If the homeowner did quit paying in year 7 for example, the house probably appreciated in value and the original loan balance has been paid down for 7 years. This is a double win for the note holder and puts you in a much stronger equity position if you ever needed to foreclose on the property.

3. Zero negotiation on price and terms: Back in the days of flipping houses, the one thing we could count on was either the Realtor, inspector, lender or the appraiser would find a way to throw a wrench into our transaction. The Realtor would try to low-ball the offer or the inspector would scare the heck out of the new home buyer with their inspection report. Regardless of the situation, we would usually end up discounting the price more than we had planned or end up dealing with more repairs than we hoped for. With owner financing, you are providing so much value for the home buyer that most of those issues just go away. We sell all of our homes “AS-IS” and our interest rate and prices are firm. We lay down the rules of the game up front and 99% of the time there are no issues. When you offer owner financing, you make the rules.

4. Supply and Demand: There are more buyers looking for owner financing opportunities than there is supply in most cities. The mistake most rookie investors make is that they take the first warm body that shows up and is willing to give them a down payment. Remember, you are trying to create headache-free, long term streams of income. We will discuss our “Character Underwriting” philosophy later in the book. For now, realize that there is a huge demand for owner financing and the wise investor patiently waits for the “right buyer” to come along.

5. Bringing value to the community: Often times when we purchase a home, the neighbors come over and start talking to us. They want to know what we are going to do with the house. When we tell them that we are going to fix up the property, they are ecstatic! Many of our homes have been the ugly duckling on the street for a long time. They also ask if we plan to rent the home or sell it. You should see their faces light up when we tell them we are going to sell the home and not rent it. The neighbors love to know that they are going to have someone in the house that will have pride of ownership, not a rotating supply of tenants.

If you would like to pre-order a copy of the book, please email Mitchell@thenotefactory.com.